Reductions in rates of interest in the course of the climax of the COVID-19 disaster in 2020 dropped the price of leveraging to historic lows. This incentivized folks to take loans and leverage their investments in order that they might maximize income with out having to liquidate their property.

Cryptocurrencies benefited vastly from this considerable liquidity within the monetary markets. The introduction of debt markets in cryptocurrencies paved the way in which for the decentralized finance (DeFi) trade to grab a larger share of the funding panorama. The worth of funds locked in several DeFi purposes and protocols exploded from a mere $600 million in January 2020 to as excessive as $180 billion in December 2021.

Because the Federal Reserve began elevating fund charges in March 2022 attributable to surging U.S. inflation, an infinite deleveraging befell within the crypto DeFi trade. As the price of leveraging has turn into costlier, the demand within the crypto market has shifted in direction of comparatively risk-off property that aren’t a part of the DeFi area.

As a consequence, the entire worth locked (TVL) in DeFi merchandise dropped to a low of $52 billion on June 19, shedding 71% from the worth highs reported in December 2021. The TVL decline is a operate of each falling token valuations, in addition to the discount in mixture leverage.

Under are the TVL drops in percentages for various DeFi merchandise in the course of the second quarter of 2022:

- Decentralized exchanges (DEX): -63%

- Lending & borrowing platforms: -71%

- Yield farms: -68%

- Liquid staking: -76%

DEXs represent the most important class within the DeFi area at $23 billion TVL as of June 30, whereas lending & borrowing platforms had $15 billion TVL on the identical date. Yield farms and liquid staking are two of the smaller classes in DeFi, with $6.5 billion and $5.5 billion TVL respectively as of June 30.

On this article, we’ll overview the notable crypto ecosystem occasions within the first half of 2022 that proceed to form DeFi area.

The collapse of UST and Terra

The collapse of the Terra protocol and its native algorithmic stablecoin, UST, was probably the most impactful occasion within the DeFi trade in the course of the second quarter of 2022.

A complete of $30 billion worth simply evaporated inside a couple of days in Could 2022, which then created a domino impact throughout the entire ecosystem. Pressured liquidations and bankruptcies snowballed till they reached a $52 billion TVL dip on June 19.

UST’s de-peg

Following the Fed’s charge hike announcement on Could 4, the value of Bitcoin began to drop quickly. UST was backed with Bitcoin reserves value $1.6 billion, so a meltdown in reserves precipitated panic amongst UST holders who rushed to promote their tokens to different stablecoin merchandise.

An unknown person on Binance offered $84 million of UST to different stablecoins whereas the identical pockets reportedly swapped a complete of 285 million UST on decentralized platforms like Curve and Anchor.

Such massive sell-offs ultimately broke UST’s peg in opposition to the US Greenback on Could 8 and there was not a lot curiosity left amongst arbitrageurs to protect the worth of UST.

Hyperinflating the LUNA provide

To counter the massively rising UST provide in circulation, the Luna Basis Guard (LFG), a non-profit group that backs the ecosystem, began to purchase UST by depleting the BTC reserves. A pockets tackle publicly related to Terra exhibits that the roughly 71,000 BTC within the reserves was exhausted attempting to save lots of UST (solely 313 BTC are current within the pockets at present).

Nevertheless, the market was already swamped with so many UST tokens that neither the depletion of reserves nor the arbitrage efforts of merchants had been sufficient to revive the peg. As a closing measure to save lots of UST, the Luna Basis Guard selected the trail of hyperinflating the LUNA token provide.

By the character of the protocol’s design, the value of UST is algorithmically backed by LUNA tokens. LUNA holders have the appropriate to mint 1 UST for each $1 value of LUNA they maintain. When UST is minted, an equal quantity of LUNA tokens is burnt and brought out of circulation.

Equally, UST holders have the appropriate to mint a corresponding quantity of LUNA tokens for each UST they maintain, which might in return take away the UST out of circulation.

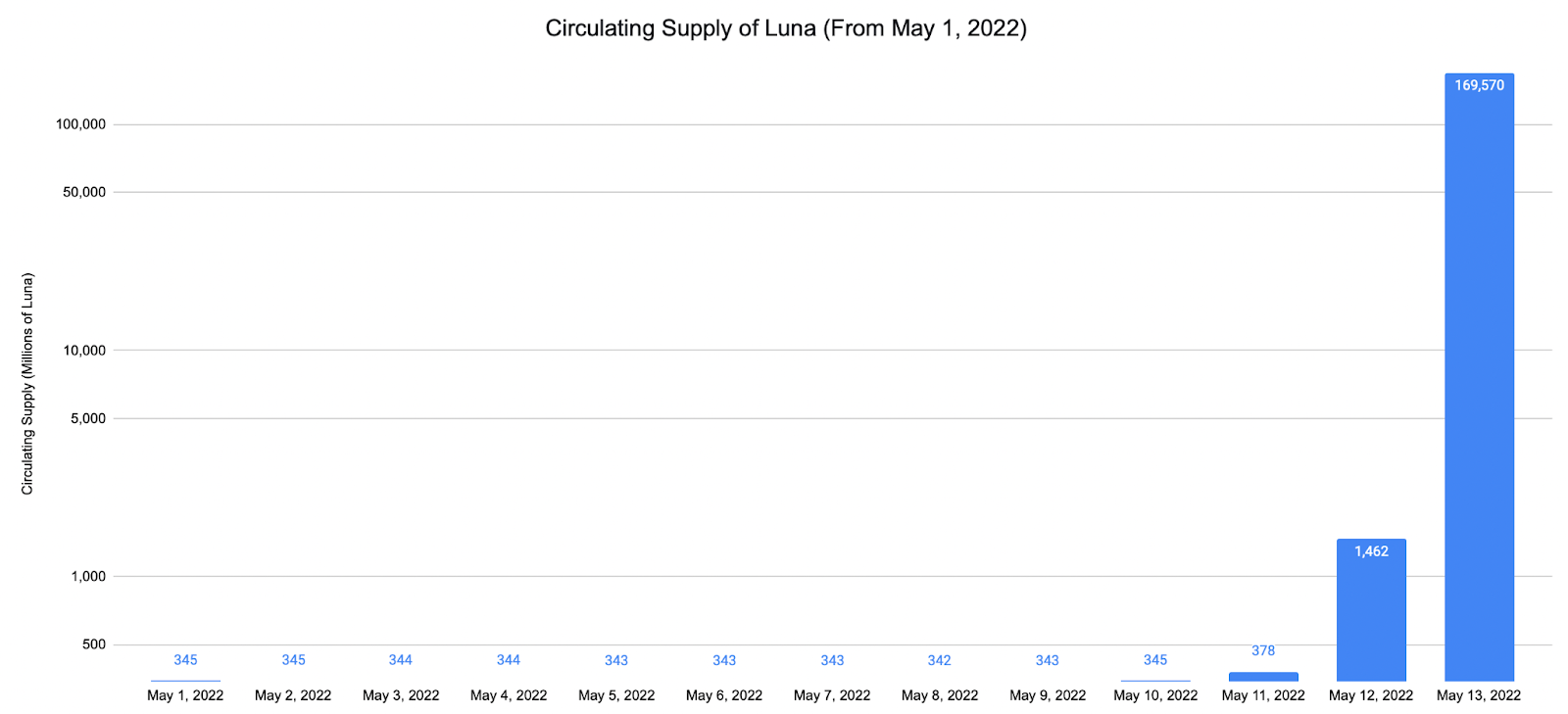

LFG minted an unbelievable quantity of LUNA tokens to lower UST’s circulating provide and push its worth again to the $1 peg.

LUNA’s one billion complete provide rose to six billion on Could 10, greater than 50 billion on Could 11, and over 6 trillion tokens by Could 13.

The beneath chart shows the large spike in LUNA’s circulating provide which was minted in a matter of three days.

Supply: Messari

In the long run, none of this LUNA printing might save the worth of UST which fell to as little as 10 cents per token on Could 13 when the Terra blockchain was lastly halted. Hyperinflation collapsed the value of LUNA from $60 to lower than one cent inside a couple of days, and exchanges concurrently stopped each Luna’s and UST’s buying and selling actions.

The aftermath

The collapse of LUNA and UST created insolvencies amongst main crypto hedge funds and enterprise capital corporations, a few of which ended with chapter.

One of many largest crypto hedge funds, Three Arrows Capital (3AC) filed for chapter in June following a British Virgin Islands (BVI) courtroom order that liquidated the fund’s BVI department property. The liquidation order got here after 3AC defaulted on a $650 million mortgage from digital asset brokerage Voyager Digital on June 27. The key set off for this insolvency was 3AC’s $560 million lengthy place in LUNA, which virtually went to zero with Terra’s collapse.

Voyager Digital additionally filed for chapter within the subsequent few weeks.

On Could 27, the Terra blockchain was forked by the order of a group vote. The brand new chain, Terra 2.0 or Terra, changed the previous one (now referred to as Terra Traditional) and exists with out UST. Most of the apps and protocols that existed on the now-Terra Traditional carried over to Terra 2.0.

Regardless of providing comparable utilities for customers as Terra Traditional did earlier than the collapse, the up to date community has to date failed to realize traction. Terra 2.0 captured about $270 million in worth as of June 30. This represents a close to 82.5% drop because it went dwell in late Could.

Ethereum block area wars

Community miners or validators on a blockchain compete for block area, which is the appropriate to create new blocks. Incomes block area requires a certain quantity of funding – both within the type of computing energy, as with mining, or by having a stake within the community’s native foreign money, which is required of validators. When a brand new block is created, miners or validators earn rewards as a return for his or her funding.

The Ethereum community has been the location of probably the most fierce block area wars within the cryptocurrency ecosystem. It is a consequence of Ethereum’s scaling points which have persevered since its launch.

The low throughput of the unique Ethereum blockchain (15 transactions per second) causes the community to get congested very simply. The demand by customers to be included within the subsequent validation block on a extremely congested community sometimes causes miners to demand astronomical transaction charges, also called fuel.

Layer 2 (L2) protocols had been launched on Ethereum as a scaling resolution. L2 protocols act as aspect roads from the principle Ethereum community to execute transaction requests. This in return reduces the load on the mainnet (layer 1, or L1) and makes transactions cheaper and sooner.

On an L2 community, transactions are recorded “off-chain” with out being acknowledged by the principle, L1 community. A person can execute any variety of transactions on L2 whereas paying for a single on-chain transaction (fuel) on the mainnet.

Charges on L2 networks are sometimes very low and the next drops in on-chain transaction hundreds considerably cut back the fuel charges on the principle Ethereum blockchain.

The share of Ethereum transactions on the mainnet has been diminishing in opposition to transactions on Optimism and Arbitrum, two of the main Ethereum L2 options. Making up lower than 4.5% of all Ethereum transactions as of 2021’s finish, transactions on Optimism and Arbitrum occupy greater than 35% as of Q2 2022.

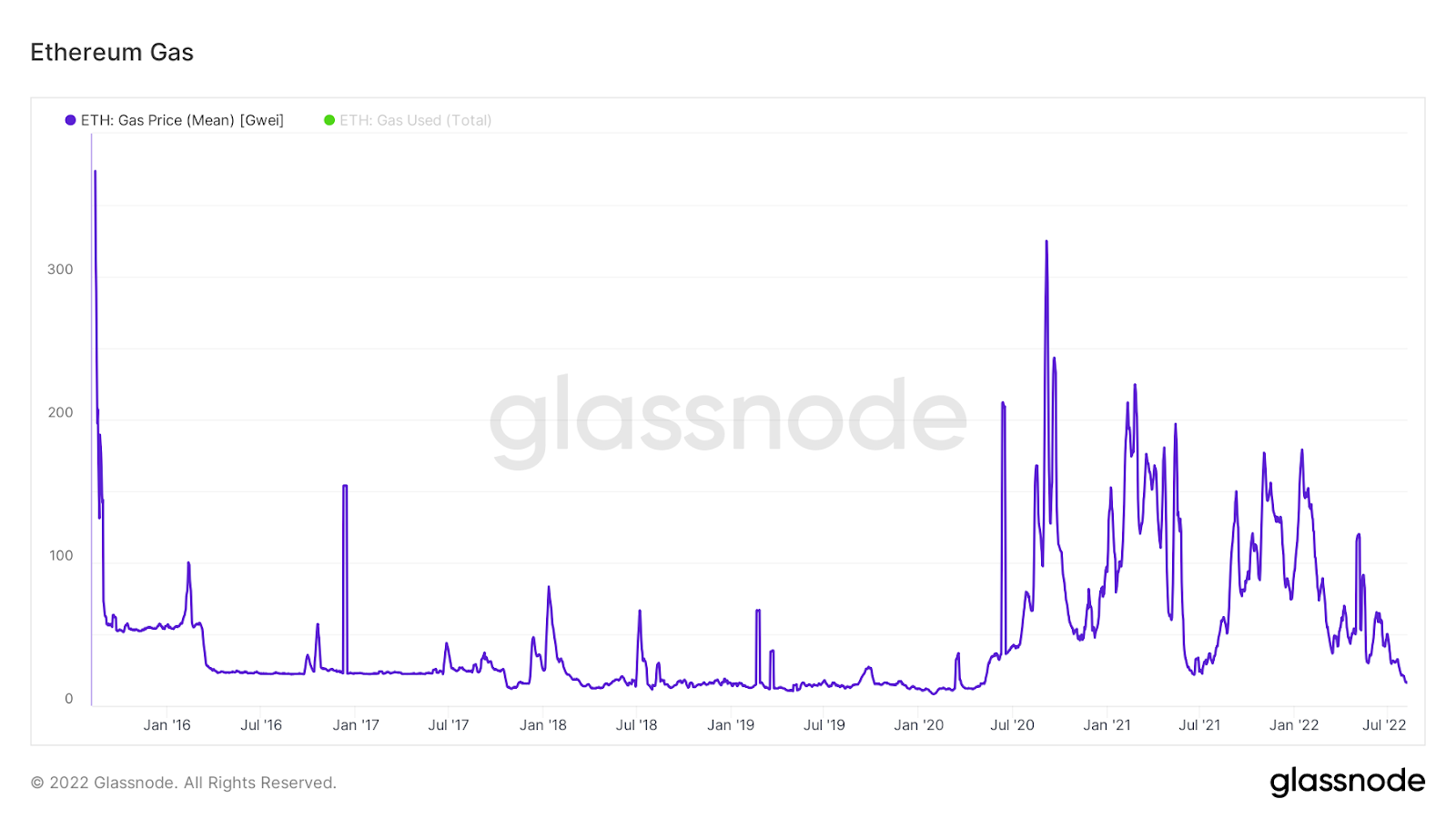

This implies 35% of all the Ethereum block area is consumed by L2 protocols. The decline in mainnet exercise considerably dropped the community income which resulted in huge Ethereum deleveraging in the course of the first half of 2022. The value of Ethereum dropped from $3,500 in December 2021 to as little as $900 on June 18. Throughout this era, the common fuel price on the mainnet dropped from over $200 in 2021 to $30 on June 19.

Ethereum fuel value chart. Supply: Glassnode

Decoupling of stETH from ETH

stETH, Ethereum’s liquid-staking token that acts as a proxy to ETH, misplaced its peg in opposition to ETH on Could 9, amidst Terra’s collapse. stETH’S most important liquidity pool on the Curve platform misplaced greater than half of its TVL in solely three days (from $4 billion on Could 9 to $1.9 billion on Could 12). As a consequence, the worth of stETH cratered to 0.88 per ETH coin on Could 13.

Liquid-staking gives liquidity for staked property by creating proxies of these property. The place staked tokens are sometimes rendered illiquid since they’re locked on the blockchain of their native cryptocurrency community, these proxies give customers full mobility whereas persevering with to earn rewards. This in return encourages development on the community the place locking property as soon as restricted their utility.

Liquid-staking tokens like stETH sometimes maintain comparable utility to the underlying staked asset (ETH) and might be deployed concurrently so as to deliver liquidity to the ecosystem.

Usually, liquid staking tokens might be swapped with the bottom staked asset which instantly releases the lock on the staked token. Nevertheless, on the Ethereum community, the ETH locked in staking contracts is inaccessible till an unknown date after the “Merge.”

Contemplating that, most individuals use stETH tokens just for leveraging their ETH staking rewards by swapping the 2 tokens forwards and backwards. Overleveraging for max rewards ultimately created an imbalance within the stETH/ETH liquidity swimming pools, the place there was not sufficient ETH to withdraw throughout turbulent occasions just like the panic promoting occasion in Could 2022.

For instance, Celsius, as soon as a serious participant within the crypto lending market, used to obtain ETH deposits from its prospects and liquid-stake them by Lido, the unique issuer of stETH. Again in Could, the corporate had over 400,000 stETH.

Nevertheless, there have been solely 148,378 ETH within the stETH/ETH Curve pool to change for 400,000 stETH tokens. In consequence, Celsius was unable to eliminate the entire stETH they personal for ETH even after draining the pool’s complete liquidity. This triggered a financial institution run for Celsius and panic promoting for stETH. Finally, the stETH/ETH peg broke and the parity traded at 0.88 on Could 13.

The outcome was an enormous liquidation occasion for stETH collaterals on DEXs and lending platforms. As stETH tokens have usually been used for leveraging, their depeg from ETH might be thought-about one other main catalyst within the DeFi market’s huge deleveraging in 2022.

Extra storms forward?

The second quarter of 2022 was characterised by antagonistic occasions that vanished the majority of the DeFi market’s progress since 2020. Taken collectively, these three occasions assist clarify DeFi’s stoop over the past quarter.

Will the market see extra de-pegs, block area wars, bankruptcies, and compelled liquidations this quarter?

Whereas black swan occasions have been commonplace within the crypto world since day one, the ecosystem continues to bounce again, and sometimes reaches new horizons. Individuals who believed within the long-term worth and use instances of crypto merchandise have usually been those that achieved the utmost returns within the cryptocurrency financial system.

Though such occasions might repeat, the large deleveraging that befell within the DeFi area – from $180 billion to $52 billion – might enable respiration room this quarter to pump some liquidity and leverage again into the system.

Hold your eyes out for additional updates and evaluation from CEX.IO because the crypto ecosystem continues to evolve. To all the time keep knowledgeable, comply with us on social media, or join our mailing checklist to by no means miss a beat.

Disclaimer: Info offered by CEX.IO shouldn’t be meant to be, nor ought to or not it’s construed as monetary, tax or authorized recommendation. The chance of loss in buying and selling or holding digital property might be substantial. It’s best to rigorously contemplate whether or not interacting with, holding, or buying and selling digital property is appropriate for you in mild of the chance concerned and your monetary situation. It’s best to consider your stage of expertise and search impartial recommendation if crucial concerning your particular circumstances. CEX.IO shouldn’t be engaged within the provide, sale, or buying and selling of securities. Please discuss with the Phrases of Use for extra particulars.

{kind=link}