Kicking off our protection of the primary earnings season of the yr for the tech trade, we as all the time begin with Intel. The blue-hued blue-chip is the primary out of the gate to report their outcomes for the primary quarter of 2023, with Intel choosing up the items after a tough finish to 2023, and a moderately painful begin to 2023. With income down on a yearly foundation nearly throughout your complete board due to a significant, trade vast droop in shopper and server gross sales, Intel’s focus has been on battening down the hatches to climate this tough interval, whereas getting ready for an eventual (if modest) upturn out there later this yr.

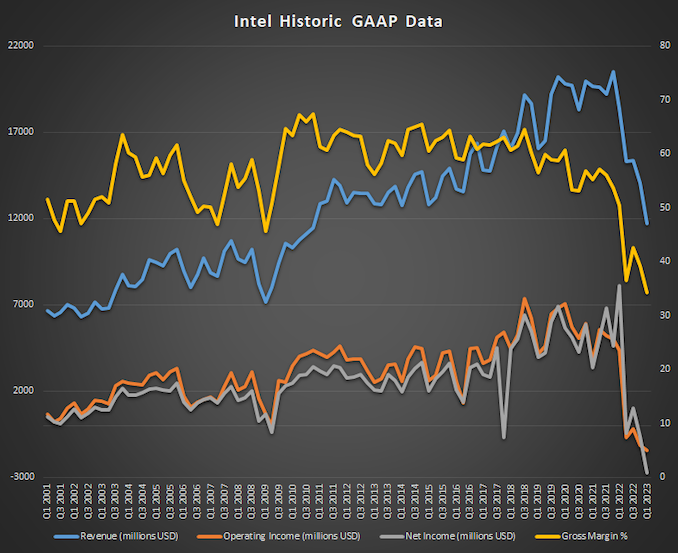

For the primary quarter of 2023, Intel booked $11.7B in income, a precipitous 36% drop from the year-ago quarter. As was the case in This autumn, Intel is within the midst of a significant trade droop, which has hit revenues exhausting and working/web incomes even more durable. Intel closed the quarter within the purple on an working revenue foundation, shedding $1.5B, and the corporate’s total web loss was a staggering $2.8B on a GAAP foundation.

| Intel Q1 2023 Monetary Outcomes (GAAP) | ||||||

| Q1’2023 | This autumn’2022 | Q1’2022 | Y/Y | |||

| Income | $11.7B | $14.0B | $18.4B | -36% | ||

| Working Revenue | -$1.5B | -$1.1B | $4.3B | -134% | ||

| Internet Revenue | -$2.8B | -$661M | $8.1B | -134% | ||

| Gross Margin | 34.2% | 39.2% | 50.4% | -16.2 ppt | ||

| Consumer Computing Group | $5.8B | $6.6B | $9.3B | -38% | ||

| Datacenter and AI Group | $3.7B | $4.3B | $6.0B | -39% | ||

| Community and Edge Group | $1.5B | $2.1B | $2.1B | -30% | ||

| Mobileye | $458M | $565M | $394M | +16% | ||

| Intel Foundry Providers | $118M | $319M | $156M | -24% | ||

In consequence, Q1’2023 is a file shedding quarter for Intel, with the corporate posting its largest loss ever recorded. Even amidst the corporate’s many ups and downs over the past 54 years, the corporate has by no means misplaced greater than a billion {dollars} in 1 / 4, not to mention over two billion. Admittedly, a part of that is structural – restructuring costs, share-based compensation prices, revenue taxes, and different non-core components contributed over $2 billion in GAAP web losses – however the measurement remains to be staggering.

Consequently, Intel’s extremely vaunted gross margin dropped to only 34.2%, its lowest in at the very least 20 years.

And but, regardless of all of this, this quarter went higher than anticipated for Intel. The corporate had warned traders early-on that it could be brutal, and whereas Intel delivered on these guarantees, it exceeded its income and EPS projections from earlier within the quarter. So whereas the corporate is much from being out of its present droop, there are some indicators that it could be nearing the underside.

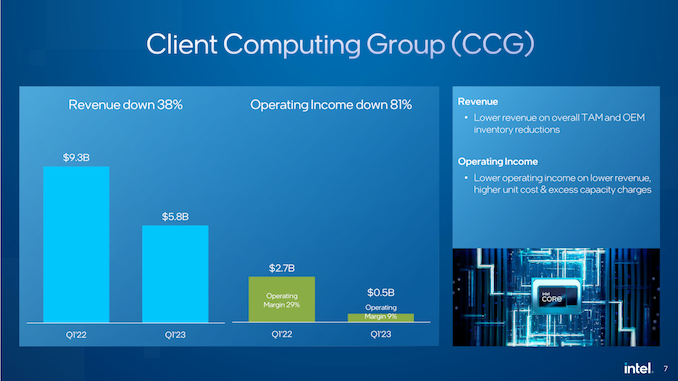

Diving into particular person section efficiency, the Consumer Computing Group (CCG) stays the bellwether for the corporate. Sadly, its additionally one of many segments being hit hardest by the tech spending downturn, with tech firms throughout the globe recalling from a 30%+ drop in PC gross sales.

To that finish, Intel booked $5.8B in shopper income for the quarter, which is down 38% from the year-ago quarter. Regardless of all of this, the CCG maintained a constructive working margin, popping out forward by $0.5B, for a 9% margin. Intel’s detailed report, laptop computer gross sales dropped more durable than desktop gross sales, although each have been down considerably. At this level Intel’s downstream OEM prospects are nonetheless burning by beforehand bought stock, which signifies that Intel is promoting far fewer chips than is common. Intel stopped offering ASP data a while in the past, so it’s unclear how a lot a change in chip pricing can be an element.

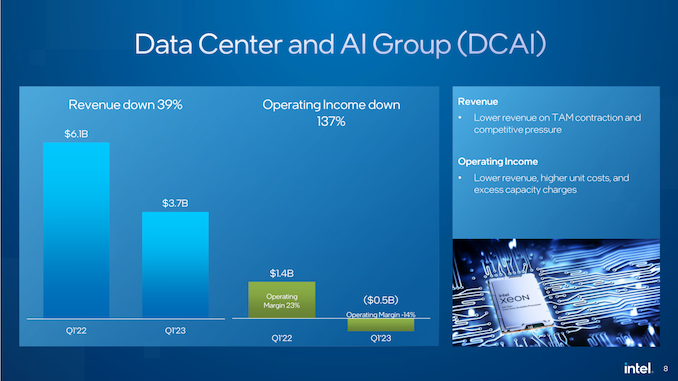

Transferring on, Intel’s Information Heart and AI Group (DCAI) is recovering from issues of its personal. Whereas Intel is now transport its long-overdue Sapphire Rapids processors in quantity, they’re nonetheless ramping up with the intention to hit their aim of 1 million chips bought by mid-year. Within the interim, DCAI gross sales have softened much more than shopper gross sales, with income dropping 39% from the year-ago quarter, regardless of Sapphire Rapids lastly being out the door.

For the quarter, Intel booked simply $3.7 billion in DCAI income. Which on an operational foundation interprets to a $518M loss for the corporate. The truth that Intel took a loss on its knowledge heart section is outstanding, though not for good causes. Whereas the information heart/server enterprise has been reconfigured a number of occasions over the past decade, I can not recollect it ever working at a loss – and checking round, this appears to be right. Regardless of being what’s historically Intel’s highest margin enterprise unit, Intel was unable to eek out even an operational revenue on server elements for the quarter.

Complicating issues considerably has been one more organizational change inside Intel. The Accelerated Computing and Graphics Group (AXG), which was beforehand a top-line enterprise unit, was cut up up and subsumed late in December by the CCG and DCAI enterprise models, with every taking their respective half of the enterprise. The fashionable incarnation of AXG is now solely centered on datacenter elements, and is part of DCAI. I convey this up as a result of as a fledgling enterprise unit, AXG itself was operating an working loss in 2022. Per Intel’s revised figures to permit for like-for-like, year-over-year comparisons with their revised enterprise models, the mixed enterprise unit shift knocked practically $300M off of DCAI’s working revenue for Q1’2022. There’s no approach to inform what the impression was for 2023, however it appears unlikely that AXG was positively contributing to DCAI’s profitability.

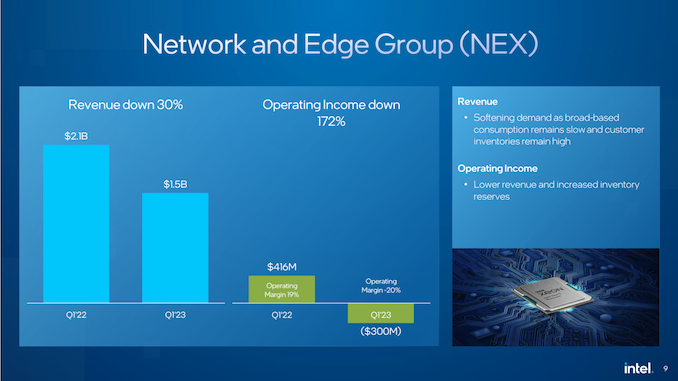

The ultimate of Intel’s large teams is the Community and Edge Group (NEX), which covers Intel’s networking, connectivity, and IoT merchandise, and is the place Intel data gross sales of different silicon equivalent to Xeon SKUs for networking merchandise. NEX has taken an analogous hit as Intel’s different top-line teams, with revenues falling 30% to $1.5B. This was sufficient of a drop to additionally push NEX into the purple, shedding $300M for the quarter. In line with feedback from Intel CEO Pat Gelsinger, the NEX buyer base is enacting comparable stock corrections as among the different chip models, which can proceed for a pair extra quarters.

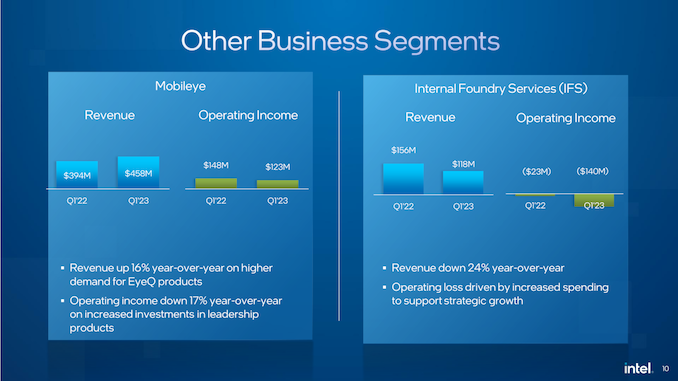

Rounding out Intel’s portfolio, Mobileye was the one distinct vibrant spot in Intel’s earnings report. The automotive group has seen income develop year-over-year by 16%, reaching new data for the quarter. And whereas working incomes have been down by 17%, it’s nonetheless working within the black. Intel Foundry Providers (IFS) then again was within the purple, although this isn’t sudden as Intel remains to be within the midst of a multi-year funding technique to retake fab efficiency management. Income dropped 24% year-over-year, however Intel has made it clear that IFS is a long-haul prospect that they may proceed to speculate closely in.

Wanting ahead, whereas Intel is indicating that elements of its enterprise segments have bottomed out (or practically so), Q1 was not the final dangerous quarter for Intel. For Q2’2023 the corporate is projecting revenues of $11.5B to $12.5B, which might be a 22% YoY drop. Gross margins are anticipated to drop additional as nicely, to a GAAP gross margin of simply 33.2%. As famous earlier, the corporate is projecting a modest restoration within the second half of the yr, however they may nonetheless must get by Q2 to get there.

Following Q1, Intel’s main total initiatives stay unchanged, each as regards to product plans and operational bills. As introduced final yr, the corporate is enterprise efforts to considerably lower bills; and in accordance with Pat Gelsinger, Intel is “nicely on our manner” in the direction of lowering prices by $3B in 2023, reaching an annual financial savings of $8B to $10B by the tip of 2025.

In any other case, Intel doesn’t have any main product launches on its public roadmap for Q2 to considerably change the established order. Nonetheless, one vibrant spot when it comes to {hardware} improvement is that Intel’s next-generation Intel 4 manufacturing course of and related Meteor Lake shopper CPU have entered manufacturing, with additional ramping happening all year long. As Intel must ship on 5 nodes in 4 years to have a critical likelihood at retaking management within the fab market, it is a promising signal that they’re certainly on monitor.

{kind=link}