Please see this week’s market overview from eToro’s international analyst staff, which incorporates the most recent market information and the home funding view.

Sturdy Huge Tech earnings can’t take away US election nervousness

Final week, Alphabet, Meta, Microsoft, Amazon, and Apple all delivered their earnings experiences for the most recent quarter. Alphabet and Amazon shocked with stronger-than-expected outcomes, whereas Microsoft dissatisfied with a warning of slower progress on account of capability constraints. Mixed, the 5 tech giants generated $450 billion in income, which they’re set to speculate closely in AI. Amazon CEO Andy Jassy even referred to it as a “once-in-a-lifetime alternative”.

Huge Tech is reportedly seeing prospects spend extra time on AI-enhanced platforms, resulting in extra advert impressions and product gross sales. This pattern justifies additional will increase in capital expenditure budgets, with a mixed run price of $250 billion per 12 months. Microsoft (in partnership with OpenAI), Alphabet, and Meta are investing closely in their very own massive language fashions, whereas Amazon and Apple select to construct on the efforts of a number of exterior suppliers.

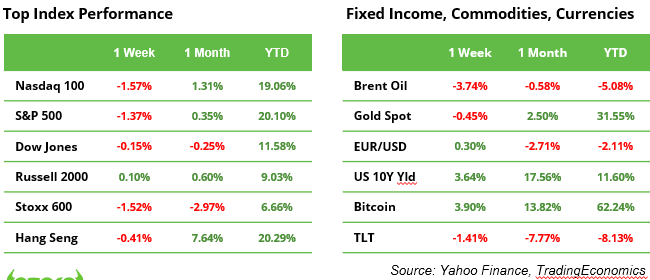

Huge Tech earnings couldn’t forestall fairness markets from retreating although. Uncertainty surrounding the result of the US elections and issues about ballooning authorities debt despatched the S&P 500 and Nasdaq down by 1.4% and 1.6%, respectively. Bond buyers demanding the next danger premium for holding authorities debt pushed the US 10-year rate of interest as much as 4.4%. Nevertheless, new macroeconomic information on progress, inflation and the roles market counsel that the Fed’s more than likely transfer this week is to chop the coverage price by 0.25%. In response to an outlook of weaker international progress and a drop in oil costs of practically 4% over the previous week, OPEC+ determined over the weekend to postpone a deliberate manufacturing improve.

The market is awaiting the US election end result earlier than selecting a route in direction of 12 months finish.

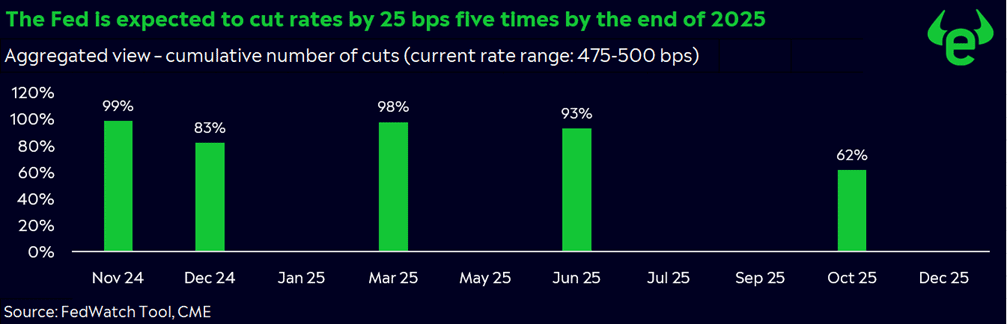

Fed seen to chop its coverage rate of interest with one other 0.25% on Thursday

The newest US financial information didn’t present a best-case state of affairs for Wall Avenue however remained acceptable for buyers, reinforcing expectations for a small Fed price minimize on Thursday. The market has practically absolutely priced in a 0.25% discount to a variety of 4.50% to 4.75%. The information pointed to a cooling labour market, barely slower progress, and stagnant core PCE inflation. Whereas these indicators help a “comfortable touchdown”, recession dangers have elevated because of this, which can lead buyers to take a position on additional price cuts within the medium time period. Fed Chair Powell’s press convention may present essential insights into the longer term course of the rate-cutting cycle.

US presidential election: will or not it’s Trump or Harris?

The result of the US elections carries important weight, because the successful candidate will set the tone for the approaching years. Nevertheless, it stays difficult to gauge how a lot a president can genuinely affect GDP progress or inventory market efficiency. Extra vital than political management is the general well being of the financial system, which at the moment positions the US comparatively strongly. The Federal Reserve retains ample flexibility to reply to surprising developments. Whereas current dangers improve vulnerability to shocks, the long-term outlook stays optimistic. Even so, the financial influence of political selections shouldn’t be underestimated.

On the core of this heated election-year debate lies tax coverage, a key difficulty sharply dividing the candidates. Republicans advocate tax cuts to stimulate financial progress, with Trump proposing a drastic 60% tariff on Chinese language imports—a dangerous transfer with potential repercussions for US shoppers. In distinction, Democrats are calling for tax hikes on the wealthiest to deal with rising revenue inequality, a shift that might profoundly influence sectors like luxurious items, telecommunications, and monetary companies.

Trump’s insurance policies may favour the defence sector, whereas a Harris victory would possibly deliver the healthcare sector into sharper focus. When it comes to vitality coverage, fossil fuels and renewables stand in stark opposition, creating uncertainty for companies. Nevertheless, there’s bipartisan consensus on the urgent want for funding in US infrastructure and on the significance of sustaining technological management over China.

Earnings and occasions

Rate of interest selections by the Fed and the Financial institution of England are the primary macroeconomic releases the market will give attention to this week. In addition to, China and Germany will publish new commerce steadiness information. All this exercise takes place on Thursday 7 November.

Many firms report earnings this week, together with 100 out the S&P 500. A range:

Earnings releases:

4 Nov. Palantir, Constellation Power

5 Nov. Ferrari, Deutsche Put up, Unicredit

6 Nov. Qualcomm, Arm, Novo Nordisk

7 Nov. Barrick Gold, Cameco, Arista Networks, Rivian, Airbnb, The Commerce Desk

Labs Partners with Fireblocks to Expand DeFi Access for Institutions")

{kind=link}