When U.S. customers have their on-line financial institution accounts hijacked and plundered by hackers, U.S. monetary establishments are legally obligated to reverse any unauthorized transactions so long as the sufferer experiences the fraud in a well timed method. However new knowledge launched this week means that for a number of the nation’s largest banks, reimbursing account takeover victims has change into extra the exception than the rule.

The findings got here in a report launched by Sen. Elizabeth Warren (D-Mass.), who in April 2022 opened an investigation into fraud tied to Zelle, the “peer-to-peer” digital cost service utilized by many monetary establishments that permits clients to shortly ship money to family and friends.

Zelle is run by Early Warning Companies LLC (EWS), a non-public monetary providers firm which is collectively owned by Financial institution of America, Capital One, JPMorgan Chase, PNC Financial institution, Truist, U.S. Financial institution, and Wells Fargo. Zelle is enabled by default for purchasers at over 1,000 totally different monetary establishments, even when an ideal many purchasers nonetheless don’t understand it’s there.

Sen. Warren stated a number of of the EWS proprietor banks — together with Capital One, JPMorgan and Wells Fargo — failed to offer all the requested knowledge. However Warren did get the requested data from PNC, Truist and U.S. Financial institution.

“Total, the three banks that supplied full knowledge units reported 35,848 circumstances of scams, involving over $25.9 million of funds in 2021 and the primary half of 2022,” the report summarized. “Within the overwhelming majority of those circumstances, the banks didn’t repay the purchasers that reported being scammed. Total these three banks reported repaying clients in solely 3,473 circumstances (representing practically 10% of rip-off claims) and repaid solely $2.9 million.”

Importantly, the report distinguishes between circumstances that contain straight up checking account takeovers and unauthorized transfers (fraud), and people losses that stem from “fraudulently induced funds,” the place the sufferer is tricked into authorizing the switch of funds to scammers (scams).

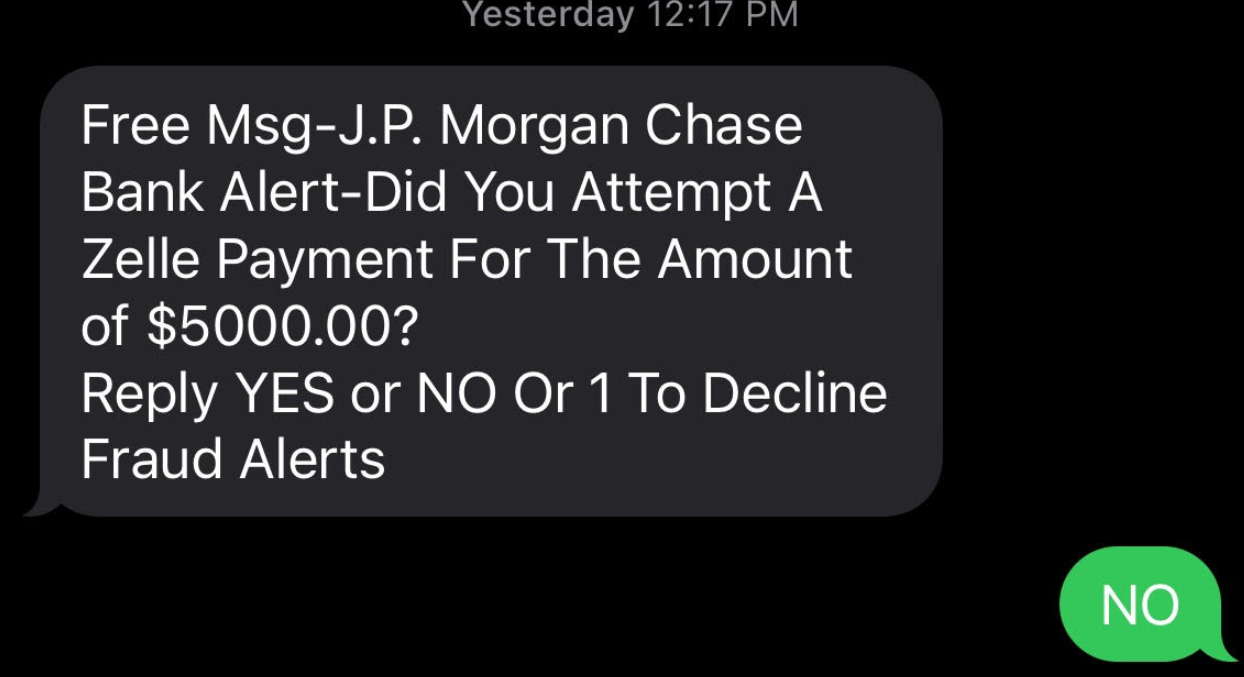

A typical instance of the latter is the Zelle Fraud Rip-off, which makes use of an ever-shifting set of come-ons to trick individuals into transferring cash to fraudsters. The Zelle Fraud Rip-off typically employs textual content messages and cellphone calls spoofed to appear to be they got here out of your financial institution, and the rip-off often pertains to fooling the shopper into considering they’re sending cash to themselves once they’re actually sending it to the crooks.

Right here’s the rub: When a buyer points a cost order to their financial institution, the financial institution is obligated to honor that order as long as it passes a two-stage take a look at. The primary query asks, Did the request really come from a certified proprietor or signer on the account? Within the case of Zelle scams, the reply is sure.

Hint Fooshee, a strategic advisor within the anti cash laundering follow at Aite-Novarica, stated the second stage requires banks to present the shopper’s switch order a type of “sniff take a look at” utilizing “commercially affordable” fraud controls that typically usually are not designed to detect patterns involving social engineering.

Fooshee stated the authorized phrase “commercially affordable” is the first cause why no financial institution has a lot — if something — in the way in which of controlling for rip-off detection.

“To ensure that them to deploy one thing that will detect chunk of fraud on one thing so onerous to detect they might generate egregiously excessive charges of false positives which might additionally make customers (and, then, regulators) very sad,” Fooshee stated. “This could tank the enterprise case for the service as a complete rendering it one thing that the financial institution can declare to NOT be commercially affordable.”

Sen. Warren’s report makes clear that banks typically don’t pay customers again if they’re fraudulently induced into making Zelle funds.

“In easy phrases, Zelle indicated that it could present redress for customers in circumstances of unauthorized transfers by which a person’s account is accessed by a nasty actor and used to switch a cost,” the report continued. “Nonetheless, EWS’ response additionally indicated that neither Zelle nor its mother or father financial institution house owners would reimburse customers fraudulently induced by a nasty actor into making a cost on the platform.”

Nonetheless, the info recommend banks did repay at the least a number of the funds stolen from rip-off victims about 10 p.c of the time. Fooshee stated he’s shocked that quantity is so excessive.

“That banks are paying victims of approved cost fraud scams something in any respect is noteworthy,” he stated. “That’s cash that they’re paying for out of pocket nearly completely for goodwill. You would argue that repaying all victims is a sound technique particularly within the local weather we’re in however to say that it needs to be what all banks do stays an opinion till Congress modifications the regulation.”

UNAUTHORIZED FRAUD

Nonetheless, on the subject of reimbursing victims of fraud and account takeovers, the report suggests banks are stiffing their clients at any time when they’ll get away with it. “Total, the 4 banks that supplied full knowledge units indicated that they reimbursed solely 47% of the greenback quantity of fraud claims they acquired,” the report notes.

How did the banks behave individually? From the report:

-In 2021 and the primary six months of 2022, PNC Financial institution indicated that its clients reported 10,683 circumstances of unauthorized funds totaling over $10.6 million, of which just one,495 circumstances totaling $1.46 have been refunded to customers. PNC Financial institution left 86% of its clients that reported circumstances of fraud with out recourse for fraudulent exercise that occurred on Zelle.

-Over this identical time interval, U.S. Financial institution clients reported a complete of 28,642 circumstances of unauthorized transactions totaling over $16.2 million, whereas solely refunding 8,242 circumstances totaling lower than $4.7 million.

-Within the interval between January 2021 and September 2022, Financial institution of America clients reported 81,797 circumstances of unauthorized transactions, totaling $125 million. Financial institution of America refunded solely $56.1 million in fraud claims – lower than 45% of the general greenback worth of claims made in that point.

–Truist indicated that the financial institution had a a lot better document of reimbursing defrauded clients over this identical time interval. Throughout 2021 and the primary half of 2022, Truist clients filed 24,752 unauthorized transaction claims amounting to $24.4 million. Truist reimbursed 20,349 of these claims, totaling $20.8 million – 82% of Truist claims have been reimbursed over this era. Total, nonetheless, the 4 banks that supplied full knowledge units indicated that they reimbursed solely 47% of the greenback quantity of fraud claims they acquired.

Fooshee stated there has lengthy been quite a lot of inconsistency in how banks reimburse unauthorized fraud claims — even after the Client Monetary Safety Bureau (CPFB) got here out with steering on what qualifies as an unauthorized fraud declare.

“Many banks reported that they have been nonetheless not dwelling as much as these requirements,” he stated. “Because of this, I think about that the CFPB will come down onerous on these with fines and we’ll see a correction.”

Fooshee stated many banks have not too long ago adjusted their reimbursement insurance policies to carry them extra into line with the CFPB’s steering from final yr.

“So that is on target however not with ample vigor and velocity to fulfill critics,” he stated.

Seth Ruden is a funds fraud knowledgeable who serves as director of worldwide advisory for digital identification firm BioCatch. Ruden stated Zelle has not too long ago made “important modifications to its fraud program oversight due to client affect.”

“It’s clear to me that regardless of sensational headlines, progress has been made to enhance outcomes,” Ruden stated. “Presently, losses within the community on a volume-adjusted foundation are decrease than these typical of bank cards.”

However he stated any failure to reimburse victims of fraud and account takeovers solely provides to strain on Congress to do extra to assist victims of these scammed into authorizing Zelle funds.

“The underside line is that rules haven’t saved up with the velocity of cost know-how in america, and we’re not alone,” Ruden stated. “For the primary time within the UK, approved cost rip-off losses have outpaced bank card losses and a regulatory response is now on the desk. Banks have the selection proper now to take motion and improve controls or await regulators to impose a brand new regulatory setting.”

Sen. Warren’s report is accessible right here (PDF).

There are, after all, some variations of the Zelle fraud rip-off which may be complicated monetary establishments as to what constitutes “approved” cost directions. For instance, the variant I wrote about earlier this yr started with a textual content message that spoofed the goal’s financial institution and warned of a pending suspicious switch.

Those that responded in any respect acquired a name from a quantity spoofed to make it appear to be the sufferer’s financial institution calling, and have been requested to validate their identities by studying again a one-time password despatched through SMS. In actuality, the thieves had merely requested the financial institution’s web site to reset the sufferer’s password, and that one-time code despatched through textual content by the financial institution’s web site was the one factor the crooks wanted to reset the goal’s password and drain the account utilizing Zelle.

Not one of the above dialogue includes the dangers affecting companies that financial institution on-line. Companies in america don’t get pleasure from the identical fraud legal responsibility safety afforded to customers, and if a banking trojan or intelligent phishing web site leads to a enterprise account getting drained, most banks won’t reimburse that loss.

For this reason I’ve all the time and can proceed to induce small enterprise house owners to conduct their on-line banking affairs solely from a devoted, entry restricted and security-hardened machine — and ideally a non-Home windows machine.

For customers, the identical previous recommendation stays the perfect: Watch your financial institution statements like a hawk, and instantly report and contest any expenses that seem fraudulent or unauthorized.

{kind=link}