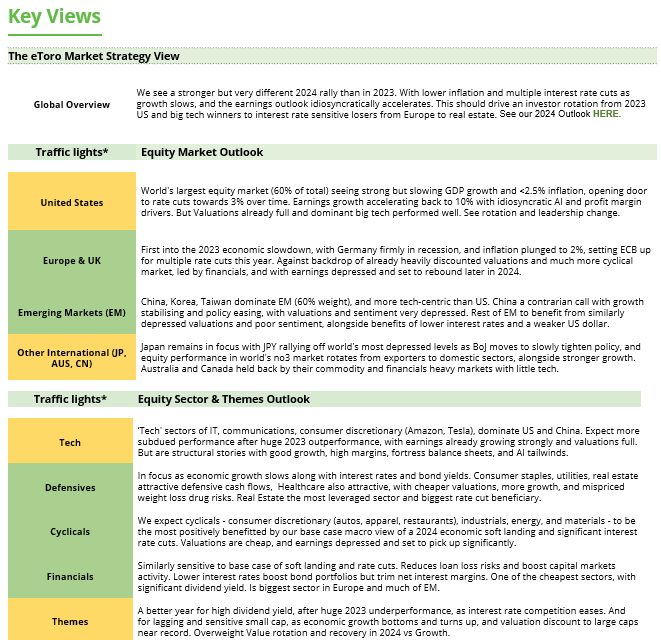

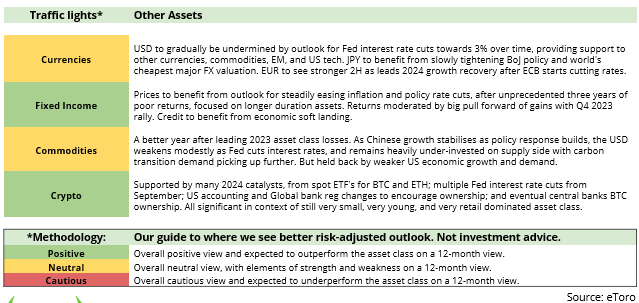

Please see this week’s market overview from eToro’s world analyst crew, which incorporates the most recent market knowledge and the home funding view.

S&P 500, Dow Jones, Bitcoin and gold all proceed to observe a optimistic development

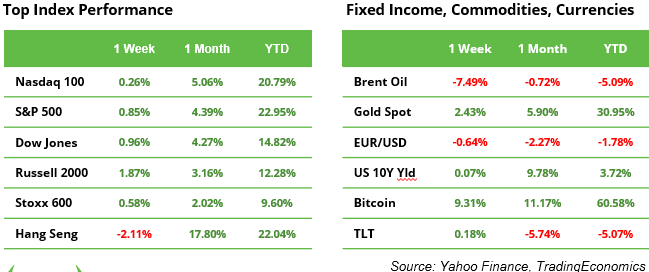

In an eventful week, the S&P 500 hit its forty seventh report excessive of the yr, whereas the Dow Jones reached its fortieth. Bitcoin gained 9%, whereas oil dropped 7%. In the meantime, gold steadily climbed above $2,700, bringing its year-to-date return to 31%.

US equities had been boosted by robust earnings from main corporations, starting from top-tier banks to Netflix, together with stable retail gross sales figures. Charge-sensitive sectors like healthcare, supplies, and industrials led the best way, as a disappointing outlook from Dutch chip machine maker ASML pushed some tech buyers towards safer choices. Nevertheless, robust earnings from TSMC reignited optimism round AI shares.

Wanting forward, 112 S&P 500 corporations, together with 7 of 30 Dow Jones constituents, are set to report their Q3 leads to the upcoming week. On Thursday, the US, Eurozone, and UK will launch new PMI knowledge, providing a snapshot of the manufacturing sector in every area. With simply two weeks till the US presidential election, expectations about potential coverage adjustments may introduce important market volatility. Within the meantime, Russia will host the sixteenth BRICS Summit.

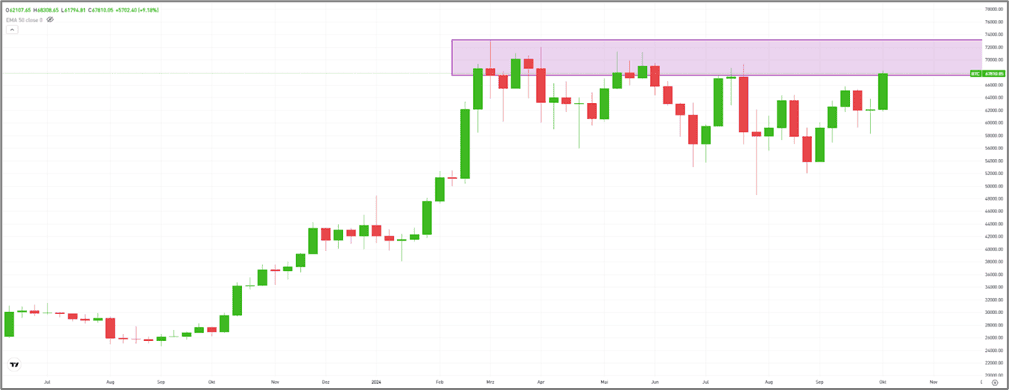

Bitcoin hodlers see themselves confirmed

After months of consolidation, Bitcoin is gaining bullish momentum. Final week, its worth surged by 9%, climbing above $68,000—simply 8% shy of its all-time excessive of $73,835, set on March 1, 2024. For a lot of holders, Bitcoin continues to function a hedge towards fiat forex devaluation, particularly as rate of interest cuts improve the cash provide and drive inflation. Institutional buyers are additionally turning to Bitcoin, which has risen 60% for the reason that begin of the yr. The rising acceptance of Bitcoin ETFs stays a big tailwind for the main cryptocurrency, doubtlessly pushing it to new report highs (see chart). As Bitcoin usually rallies as soon as key ranges are breached, FOMO (concern of lacking out) might set in on the subsequent peak.

A thought experiment: What if each investor allotted simply 1% of their portfolio to Bitcoin?

Chart: Bitcoin is testing a key resistance zone between $68,000 and $73,000

Russia hosts 16th BRICS Summit in Kazan

Talks of a brand new world order are set to accentuate this week because the BRICS international locations convene for his or her sixteenth Summit in Kazan, Russia, from October 22 to 24. The founding nations, Brazil, Russia, India, China, and South Africa, will likely be joined for the primary time by new members Egypt, Ethiopia, Iran, and the UAE, together with representatives from two dozen different international locations contemplating membership. BRICS goals to ascertain a substitute for the G7 and IMF (assembly this similar week), specializing in sanction-proof financing by selling commerce in native currencies moderately than counting on the US greenback. Whereas fast change is just not anticipated, momentum is constructing that might ultimately problem the dominance of the US greenback and the worth of US Treasury bonds, elements that partly clarify the current rise in gold costs. Nevertheless, the BRICS nations usually have conflicting pursuits and don’t at all times see eye-to-eye.

US, UK and Eurozone to launch PMI knowledge for October

Why does it matter? Manufacturing on each side of the Atlantic faces fierce competitors from China, which is making an attempt to export its approach out of a property disaster. Every area has its personal challenges: Europe is making an attempt to revive its financial system, whereas the US goals to keep away from a tough touchdown. In each instances, buyers are eager to keep away from additional declines within the PMI Composite, significantly in manufacturing. Consensus estimates put the Eurozone PMI Composite at 49.7, marginally up from 49.6 in September. Within the US, PMI Manufacturing is anticipated to get well to 48.2 from 47.3 the earlier month. Disappointing outcomes may reignite recession fears, although rate of interest cuts in each areas present some cushion towards worsening financial situations. However, stronger-than-expected knowledge may cut back the chance of additional fee cuts.

Earnings and occasions

Tesla will likely be in focus after a lacklustre robotaxi occasion with out numbers. Normal Motors and Mercedes-Benz will present one other have a look at the automotive sector. Hermès and Kering will likely be watched particularly after the disappointing LVMH figures final week.

Earnings releases:

21 Oct. SAP

22 Oct. GE Aerospace, Danaher, Verizon, Texas Devices, RTX, Normal Motors, L’Oreal

23 Oct. Tesla, Coca Cola, IBM, ServiceNow, NextEra Power, AT&T, Boeing, Iberdrola, Kering

24 Oct. Unilever, RELX, Unicredit, Hermes, Honeywell

25 Oct. Mercedes-Benz

{kind=link}