Please see this week’s market overview from eToro’s international analyst group, which incorporates the newest market information and the home funding view.

New inflation information fosters a “higher-for-longer” sentiment,

Hotter than anticipated US inflation numbers formed market dynamics. The Shopper Value Index (CPI) rose to 2.7% from 2.6%, whereas the Producer Value Index (PPI) climbed to three.0% from 2.6%, marking the largest improve since February 2023. These figures prompted bond buyers to push the yield on the US 10-year Treasury bond from 4.15% to 4.40%, reflecting a “higher-for-longer” price outlook.

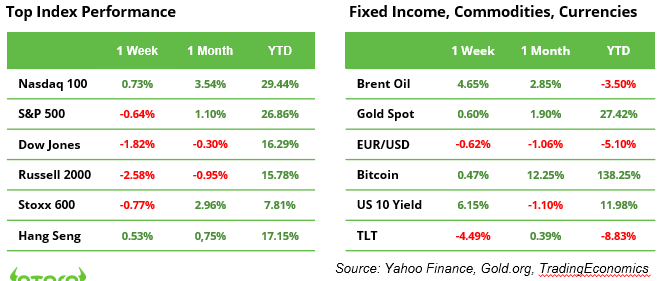

Fairness markets responded to the inflation information with blended actions, partially reversing latest developments. The small-cap Russell 2000 Index dropped 2.6%, and the value-heavy Dow Jones Index declined by 1.8%. Nonetheless, the Nasdaq 100 gained floor, pushed by sturdy performances from Google, that made headlines with a breakthrough in quantum computing, and Broadcom, that projected $90 billion in income from customized AI chip by 2027, reigniting a rally in AI shares.

Within the commodities market, oil costs surged 4.7%, whereas cocoa spiked 17%, as unfavorable local weather situations threatened the upcoming harvest and pressured current contracts.

Fed, BoJ and BoE to announce their rate of interest selections

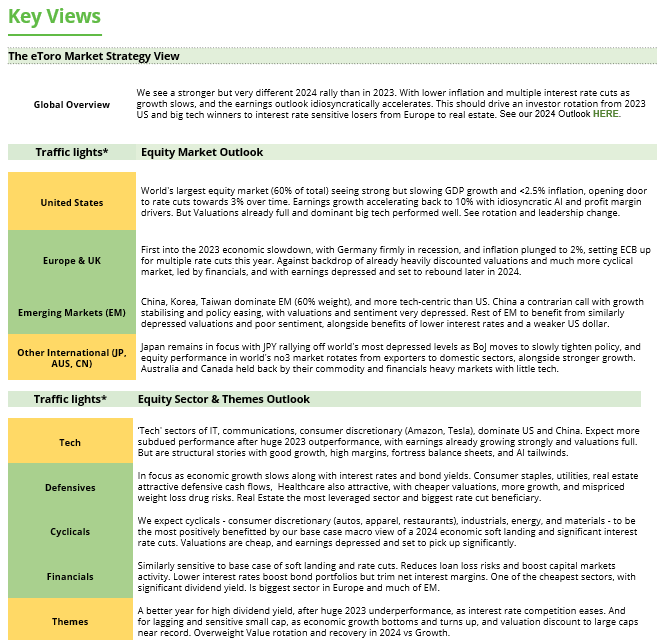

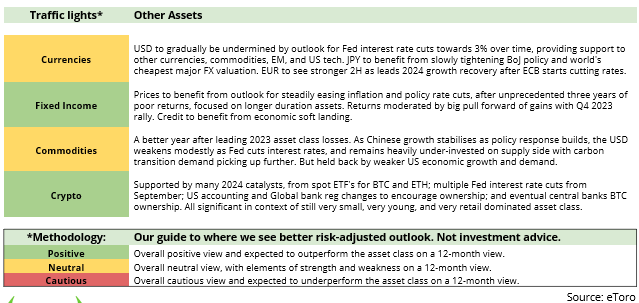

Following final week’s price cuts by the ECB and SNB, (SNB stunning markets with a 0.50% “jumbo” reduce), consideration now shifts to the Ate up Wednesday and the BoJ and BoE on Thursday. The US Federal Reserve is predicted to chop charges by 25 foundation factors to a spread of 4.25% to 4.50%, a call priced in by the market with a 96% likelihood. Nonetheless, a Bloomberg survey signifies that the Fed’s rate-cutting path will seemingly decelerate in 2025. The up to date dot plot and Jerome Powell’s press convention are anticipated to offer worthwhile insights.

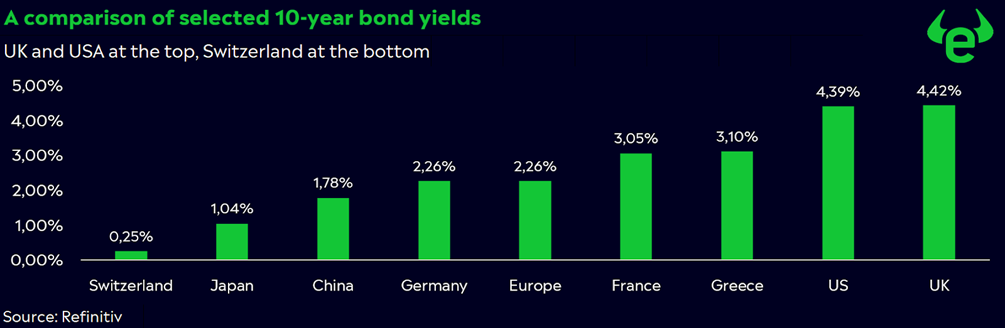

There’s a sturdy correlation between rates of interest and bond yields. 10-year bond yields globally (see chart), UK and US lead the pack. Within the US, Trump’s debt insurance policies stay a focus. In Europe, political crises in France and Germany dominate consideration. In the meantime, China’s 10-year bond yield hit a document low, with solely Japan and Switzerland providing decrease yields.

Bonds stay a worthwhile addition to portfolios for stability. Nonetheless, their long-term return potential is considerably decrease than that of equities. Greater returns within the fastened earnings markets are at the moment solely achievable with high-risk bonds.

Can the US Manufacturing PMI Break By 50?

US financial information dominates this week, with Monday’s PMI figures in focus. The Providers PMI is predicted to dip barely from 56.1 to 55.7, whereas Manufacturing PMI is forecast to rise modestly from 49.7 to 49.8. A breach of the 50 mark might sign the top of the sector’s recession. Later within the week, retail gross sales information and PCE inflation figures will present additional clues on the economic system’s route.

Musk’s profitable funding in Trump

Elon Musk, the world’s wealthiest man, invested at the least $274 million in Donald Trump’s election marketing campaign. Past monetary contributions, Musk performed an energetic function in influencing public opinion, together with his election-related posts on X garnering an estimated 17 billion views.

Was it a very good funding? Within the brief time period, it seems so. Tesla’s inventory, the place Musk owns a 13% stake, surged over 70%, including $80 billion to his web price. The influence prolonged past Tesla. SpaceX, the place Musk holds a 42% stake, noticed its valuation soar to $350 billion final week, up from $210 billion in June. Moreover, Musk’s different ventures, together with Neuralink, X, and xAI, are reported to have skilled important valuation will increase since 5 November.

The subsequent key query for buyers is how Trump’s insurance policies will influence Musk’s numerous portfolio of companies. As the brand new administration takes form, market watchers will carefully monitor potential regulatory and financial shifts that might have an effect on Musk’s wide-ranging ventures.

Which inventory markets outperformed the US in 2024?

The Nasdaq 100 Index delivered a 29% return, and the broader S&P 500 Index gained 27% thus far in 2024 (see desk). Whereas few markets have outperformed these spectacular figures, a handful stand out. Argentina and Pakistan’s inventory markets have surged by roughly 70% this 12 months. The International X MSCI Argentina ETF, listed in USD, benefited from profitable reforms beneath the Milei authorities, which targeted on cost-cutting measures and curbing inflation. Equally, the Xtrackers MSCI Pakistan Swap ETF, listed in EUR, posted sturdy good points, pushed by inner reforms and the best ranges of international funding inflows since 2014.

Earnings and occasions

Macro: PMI (16/12) Retail Gross sales (17/12), Fed (18/12), BoE, BoJ (19/12). PCE inflation (20/12)

Earnings: Micron, Lennar (18/12), Nike, Fedex (19/12)

{kind=link}