- Lululemon’s robust development has made it the second most precious sportswear model globally, pushed by worldwide demand, and a loyal buyer base.

- Regardless of latest positive aspects, Lululemon’s valuation stays comparatively low in comparison with friends, suggesting potential upside if development continues.

- Nevertheless, dangers from competitors, shifting shopper developments, and financial uncertainties might influence its development trajectory.

After rising by over 10% since its final earnings report, Lululemon overtook Adidas to grow to be the world’s second most precious sportswear producer. What many wrote off as a inventory previous its prime is wanting extra like a diamond within the tough. Whereas most retailers battle with weak shopper developments and international financial uncertainty, Lululemon continues to face out.

This athleisure designer is retaining its top-line development going, propelled by new designs, retailer expansions, and surprisingly robust demand in China. Couple that with a loyal, higher-income shopper base, and you’ve got the recipe to defy business developments.

However after its newest rally, buyers should ask: Is that this yoga-based model priced for perfection, or is there nonetheless room to develop?

What does Lululemon do?

Lululemon Athletica remodeled from a distinct segment yoga-wear model into a world athleisure participant, providing a variety of merchandise—from technical athletic clothes and footwear to health equipment—for each women and men.

Lululemon embraced e-commerce and made on-line gross sales a key a part of its technique and enabled the model to broaden its footprint. Its distinctive strategy to advertising – creating a way of group and belonging made Luluemon not only a model, however a life-style. This has been a profitable playbook for a lot of manufacturers.

How is administration dealing with development?

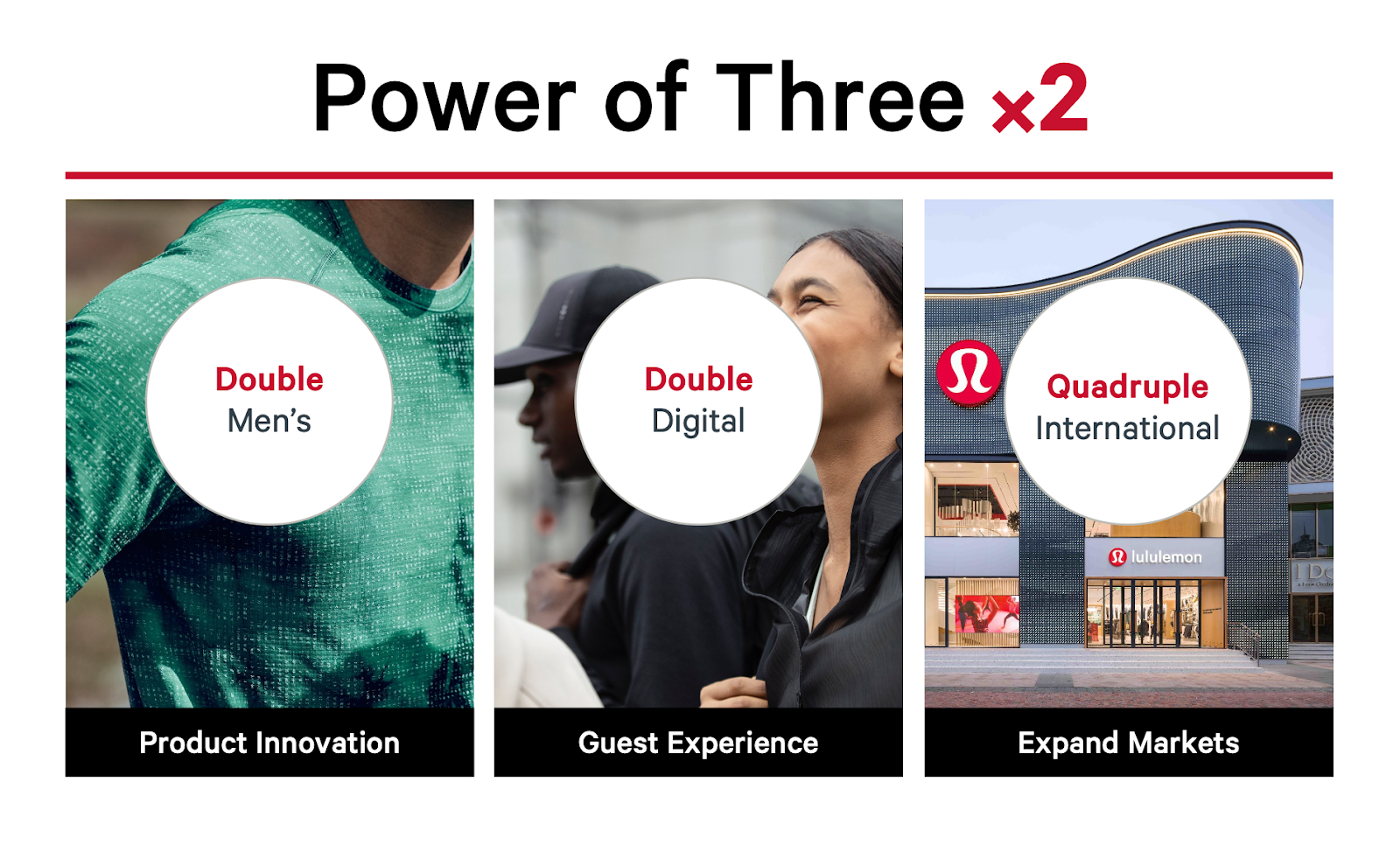

Lululemon is executing its Energy of three×2 plan, which laid out targets in 2021 to double three KPI’s by 2026.

(lululemon.com)

Firstly, Lululemon plans to double males’s income by 2026. It’s utilizing its confirmed mannequin of technologically superior premium materials to ascertain itself in males’s operating, coaching, and yoga, whereas increasing into new classes corresponding to tennis, golf and mountaineering and tapping into footwear and equipment.

Secondly, the model doubled down on e-commerce and intends to double on-line revenues by 2026. They’ve a stable basis already. Over 39% of gross sales are completed on-line and Lululemon has over 24 million membership customers, reinforcing its group strategy.

Thirdly, the corporate plans to quadruple international income from 2021. It has vital alternatives to broaden globally, having not too long ago entered China and began growth into EMEA and APAC. Out of its 749 shops, 138 are in China, 47 in Emea and 105 in APAC, establishing a foothold in these markets and creating additional alternatives for Lululemon.

The place Lululemon is missing

Expert administration is the important thing to success on this planet of trend. Beneath the present CEO, the corporate has been increasing, however it got here at a price. Luluemon has misplaced a few of its luster with a scarcity of innovation, or what the corporate calls “newness”. It recognized and began engaged on the difficulty, managing to barely revive development within the final quarter, significantly within the troublesome ladies’s phase.

We have now to say the U.S., the place comparable gross sales have been down -3% for the primary time final quarter. Weakening shoppers have dragged on many companies, and it was time for Lululemon to really feel the sting.

This scary pattern has considerably reversed course as income development elevated to 2% YoY and comparable gross sales declined -2% as in comparison with -3% final quarter. It stays to be seen if it is a long-term restoration trajectory or a seasonal blip, however administration was constructive about US development on the earnings name. Bettering macroeconomic circumstances might present a lift to gross sales in 2025.

Quarterly beat spurred investor optimism

The December 2024 quarterly report confirmed an organization nonetheless in development mode. Internet income for Q3 FY2024 reached $2.4 billion, representing a 9% year-over-year improve. This top-line growth was fueled by a mixture of retailer openings, enhancing e-commerce penetration, and profitable product launches within the males’s and footwear classes. Comparable gross sales rose 3%, with gross margins of 58.5%.

Earnings per share (EPS) got here in at $2.87, a notable enchancment from $2.53 in the identical interval final yr. The corporate additionally raised its full-year income steerage from a variety of $9.5 billion to $9.7 billion, reflecting administration’s confidence in sustaining this momentum.

China: Why Lululemon is excelling the place others battle

Gross sales in China surged by 40% within the first two quarters – with costs 20% larger than within the U.S. This can be a hanging demonstration of Lululemon’s pricing energy.

Whereas many Western retailers are going through points in China amid altering shopper preferences and fierce native competitors, Lululemon is bucking the pattern. China gross sales surged by roughly 25% this quarter, outpacing development in nearly each different geography. So what’s the key?

Lululemon’s model message of wellness, high quality, and premium craftsmanship resonates with Chinese language shoppers who worth authenticity and life-style over discount pricing.

Moreover, the corporate has localized its strategy, partnering with native health influencers, internet hosting group yoga occasions, and providing merchandise tailor-made to the preferences and local weather of Chinese language cities. Mixed with Lululemon’s digital technique—leveraging Chinese language social media platforms and integrating with native e-commerce giants—allows it to fulfill shoppers the place they store. This strategy has allowed the corporate to maintain its Chinese language operations rising.

Is Lululemon undervalued?

(koyfin.com)

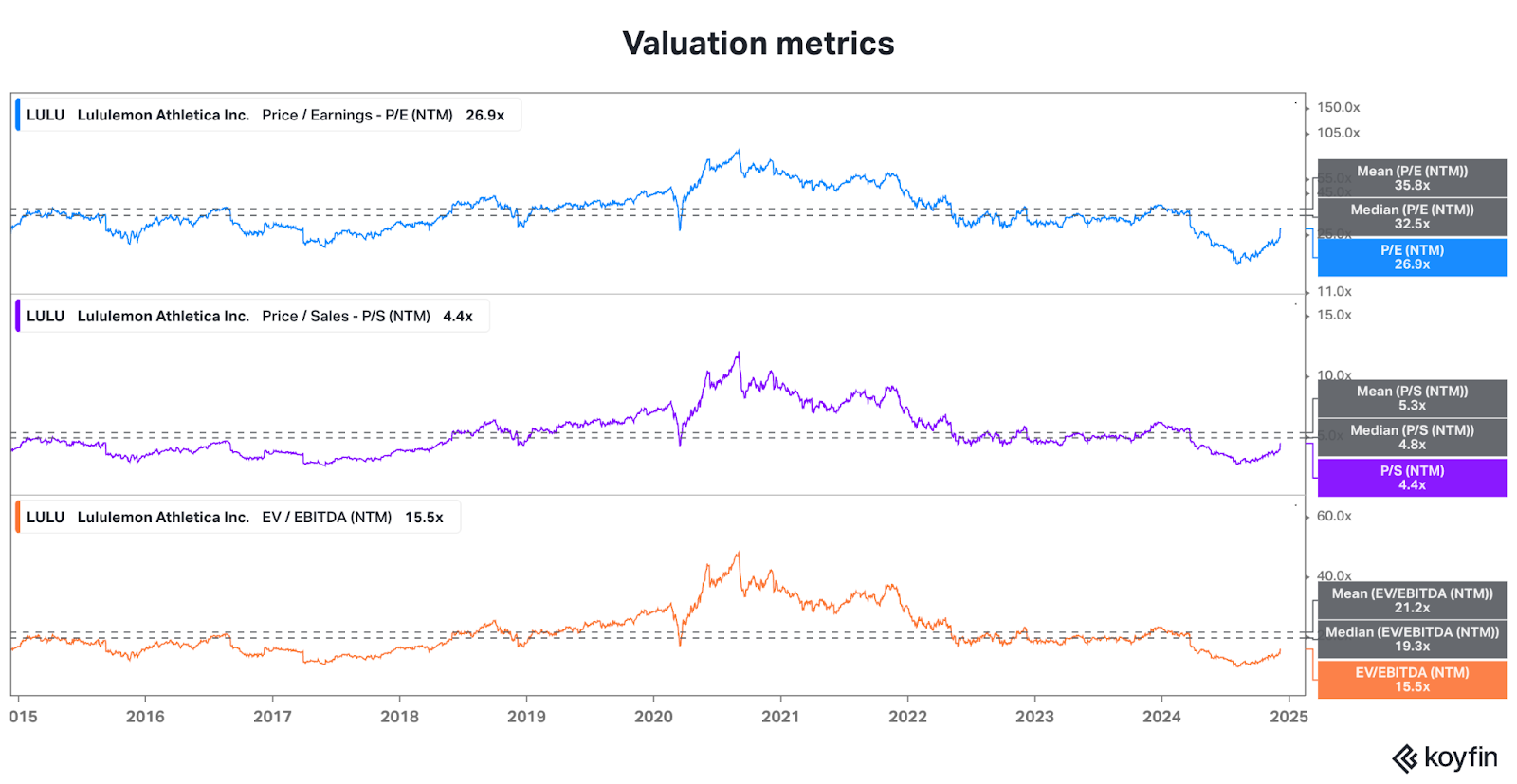

Because of revenues rising 21% p.a. over the previous 10 years, Lululemon’s inventory was given a premium valuation. After development collapsed in 2023, the valuation turned its enemy, and the inventory collapsed over 50% from its highs as buyers feared that Lululemon’s development was completed for good. However with each income and earnings development outpacing estimates and rising in Q3, investor sentiment has improved. Proper now, the corporate’s P/E ratio stands at 27.43, which signifies about 20% upside from right here to the historic median.

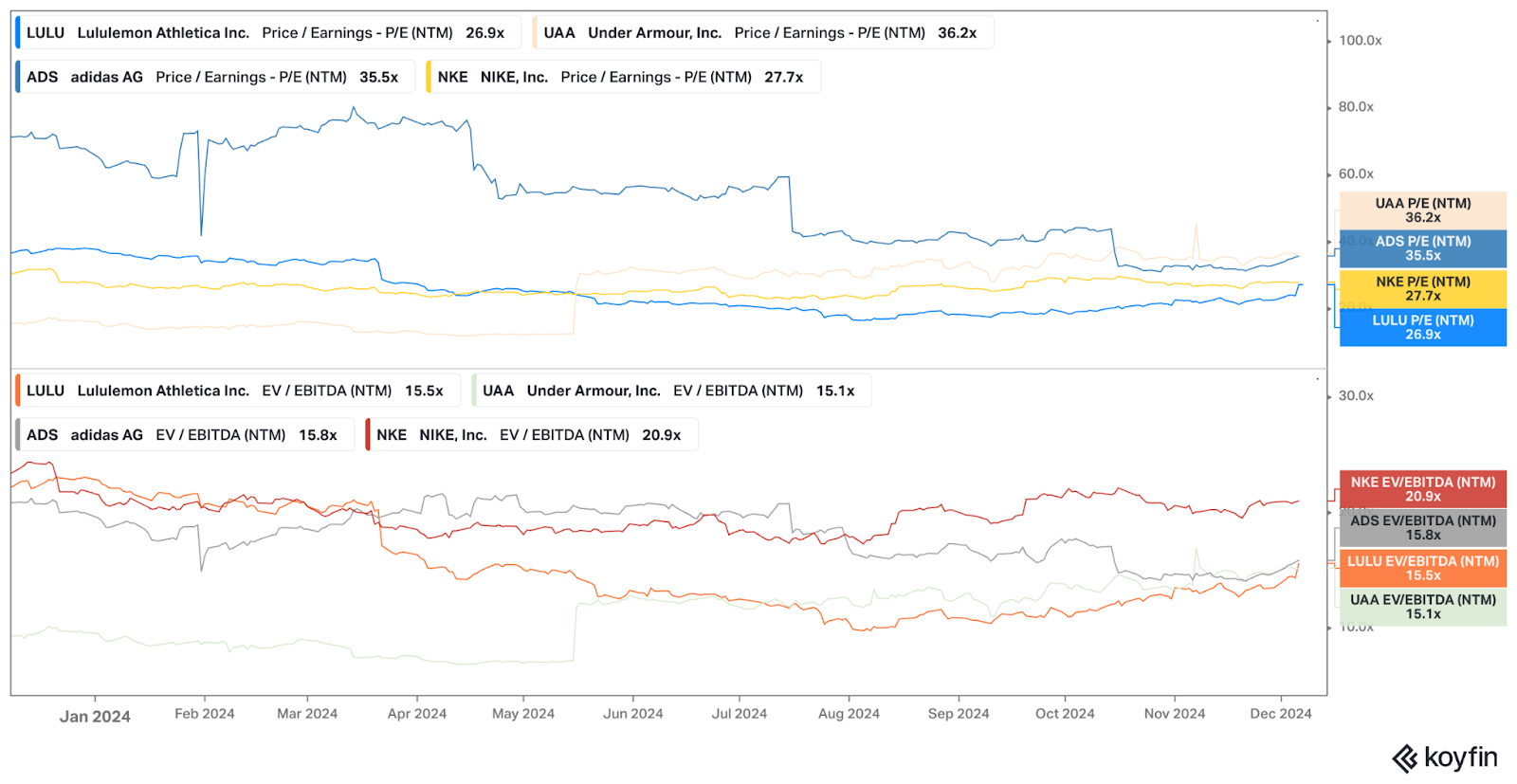

Wanting on the valuation of its friends, we are able to see that regardless of robust efficiency, Luluemon’s inventory remains to be buying and selling on the low finish of the group. This may replicate much less urge for food from buyers, but additionally create a possibility for the corporate to to develop if it proves itself to the market.

(koyfin.com)

Let’s take a look at three potential eventualities to see how Luluemon’s valuation stacks up:

- Bull Case: Lululemon continues to develop earnings by 15%+ yearly over the subsequent 5 years, pushed by geographical growth and sequential development and margin enchancment due to a stronger shopper. On this situation, long-term shareholders may reap vital rewards.

- Impartial Case: Development moderates to round 10% per yr as markets like North America strategy saturation and China’s development normalizes. If margins keep robust, the valuation might compress to replicate slowing development. Whereas the aggressive evaluation means that Lululemon’s inventory might continue to grow, I might not count on explosive positive aspects.

- Bear Case: Weak spot in China catches as much as Lululemon, whereas slower international financial restoration may inhibit growth. American shoppers keep weaker because of larger charges for longer. Margins may face strain from competitors and better enter prices. The valuation may compress and depart buyers with a stagnating or slowly declining inventory.

For buyers, it’s vital to gauge how international macroeconomic circumstances evolve and the way they may have an effect on the expansion trajectory towards excessive multiples. Lululemon might proceed to outperform, but when development stumbles, the inventory might face a harsh valuation reset.

What dangers is Lululemon going through?

Even the strongest manufacturers face challenges. For Lululemon, dangers embrace elevated competitors from established names like Nike, Adidas, and rising direct-to-consumer manufacturers that might chip away at market share corresponding to Alo Yoga or Vuori.

Shopper preferences in trend and health can shift quickly, and Lululemon’s premium pricing may depart it weak if financial circumstances tighten and consumers start to commerce down. There’s already a rising pattern of dishevelled outsized clothes as in comparison with the glossy, determine enhancing model of Lululemon’s merchandise.

Provide chain disruptions, rising materials prices, or sudden geopolitical tensions might additionally dampen development, particularly due to the danger of commerce wars with China.

Outlook for the enterprise

Lululemon stands at a juncture. The corporate’s newest quarterly outcomes present no signal of slowing down, with development firing on a number of cylinders. However we can’t ignore the truth that Lululemon is a standout within the business. It’s questionable whether or not the corporate can be a diamond within the tough, or if shopper weak point simply hasn’t caught as much as this model but. Buyers have to determine whether or not they’re snug paying prime greenback for development that depends upon persevering with stabilization of financial circumstances.

For long-term buyers who imagine within the premium model, the inventory could also be a purchase. However for those who choose conservative bets, ready for a greater entry level is likely to be your greatest yoga pose. Ultimately, Lululemon stays a beautiful enterprise, however within the attire business, success could be fleeting.

{kind=link}